Munis were slightly firmer in spots Wednesday with more of the focus on the primary, including a large taxable California general obligation bond sale in the competitive market, while U.S. Treasuries were better and equities ended the session up.

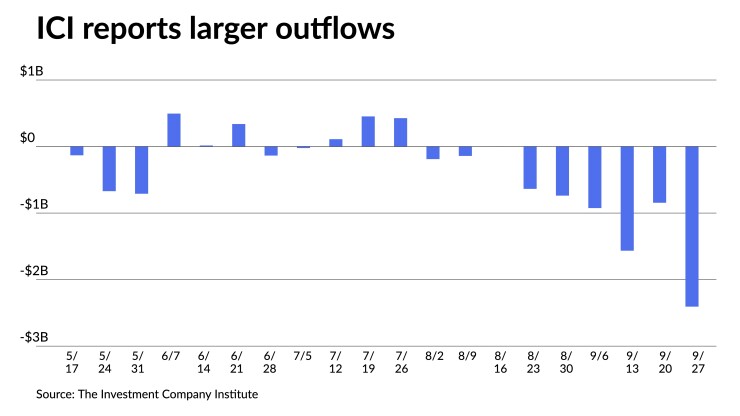

The Investment Company Institute Wednesday reported investors pulled $2.407 billion from municipal bond mutual funds in the week ending Sept. 27 after $845 million of outflows the previous week. This is the second-largest outflow cycle of 2023, only being surpassed by outflows of $3.157 billion for the week ending Jan. 4.

For the most recent reporting week, ETFs saw outflows of $136 million after $462 million of inflows the week prior, according to ICI.

While munis were bumped up to three basis points Wednesday, depending on the scale, triple-A curves have been selling off for the past two weeks.

The two-year muni-to-Treasury ratio Wednesday was at 72%, the three-year was at 72%, the five-year at 73%, the 10-year at 74% and the 30-year at 90%, according to Refinitiv Municipal Market Data’s 3 p.m., ET, read. ICE Data Services had the two-year at 71%, the three-year at 73%, the five-year at 71%, the 10-year at 73% and the 30-year at 89% at 4 p.m.

The recent selloff is “having multiple impacts across the market at a point in the calendar when seasonality can play a larger role in performance,” said Kim Olsan, senior vice president of municipal bond trading at FHN Financial.

A growing number of delayed new issues is a “byproduct of higher rates impeding the economics of refunding plans,” she said.

Across several credits, she said around $1.2 billion of pricings have moved on day-to-day status.

“In a month’s time when these issues would have begun preparations for pricing, the yield curve has seen a 50-60 basis point spike,” she said.

What may result, Olsan noted, “is a more manageable weekly figure that helps smooth out distribution amidst rate volatility.”

Last October saw the smallest monthly issuance total at $28.7 million for the month in a decades as yields rose, “a potential harbinger of the current market,” she said.

Furthermore, muni operators are dealing with “where to position along the curve with a modest inversion still in place out to 12 years — namely, take the higher yields with limited lockout or extend for 50 basis points more yield into the longer intermediate range.”

A barbell approach of 1-2 year effective dates and 12-15 year final maturities seems to be happening.

Examples include “PSF-backed Pearland TX Independent School 5s due 2032 (callable 2026) at 4.00% and Aa1/AA+ New York Dormitory Authority Personal Income Tax 5s due 2035 (callable 2025) at 5.03% speak to the exaggerated yields in place for short-optioned bonds,” according to Olsan.

Similarly, she said “new issue Aa2/AA Omaha NE Public Power bonds were priced with a 5% due 2038 (10-year lockout) at 4.24%.”

The yield backup “brings to light the pressure on liquidity and the work in progress to find an equilibrium between sellers and buyers,” she said.

Bid wanteds were above $2 billion Tuesday, which is the highest of the year.

Despite recent adjustments, she said the 10-year Refinitiv MMD has a while to go before it tops the high of 4.31% from October 2008, but the 10-year UST is at a new yield high in that period.

“Of note is the improvement in relative values that is factoring into allocations, where a mid-70% ratio has developed in intermediate maturities,” she said.

The absolute 10-year yield point is “nearly 150 basis points off the 2023 low — not totally negating higher relative values but playing more of an equal role from the period of extremely low rates,” Olsan noted.

In the primary market Wednesday, the largest deal of the day sold in the competitive market. California (Aa2/AA-/AA/) sold $502.850 million of taxable general purpose GOs, Bid Group A, to J.P. Morgan, with 5.5s of 10/2028 at 5.17% and 5.75s of 2031 at 5.57%, noncall.

The state also sold $440.545 million of taxable general purpose GOs, Bid Group B, to Wells Fargo Bank, with 11s of 10/2033 at 5.65% and 5.875s of 2041 at 6.05%, callable 10/1/2033.

In the negotiated space, Citigroup Global Markets priced for the Tennessee Housing Development Agency (Aa1/AA+//) $305 million of non-AMT social residential finance program bonds, Issue 2023-3A, saw 3.9s of 7/2024 price at par, 5s of 1/2028 at 4.15%, 5s of 7/2028 at 4.20%, 4.7s of 1/2033 at par, 4.75s of 7/2033 at par, 4.95s of 7/2038 at par, 5.2s of 7/2043 at par, 5.35s of 7/2048 at par, 5.4s of 7/2053 at par and 6.25s of 1/2054 at 4.97%, callable 7/1/2032.

J.P. Morgan priced for South Carolina’s Building Equity Sooner for Tomorrow (Aa2///) $278.835 million of installment purchase revenue refunding bonds on behalf of the Greenville County School District, with 5ss of 12/2024 at 3.92% and 5s of 2028 at 3.65%, noncall.

Ramirez & Co. priced for the New York State Housing Finance Agency (Aa2///) $149.575 million of affordable housing sustainability revenue bonds. The first tranche, $14.895 million of 2023 Series D-1, saw all bonds pricing at par: 3.75s of 11/2024, 4.05s of 11/2028, 4.55s of 11/2033, 4.95s of 11/2038, 4.95s of 11/2038, 5.1s of 11/2043, 5.25s of 11/2048, 3.5s of 11/2053, 5.35s of 11/2058 and 5.4s of 5/2063, callable 6/1/2032.

The second tranche, $134.680 million of 2023 Series D-2, saw 4.5s of 11/2062 with a mandatory tender date of 11/1/2028 price at par, callable 11/1/2025.

BofA Securities priced for Riverside County $103.330 million of Teeter Plan obligation notes, 2023 Series A, with 3.875s of 10/2024 at 3.70%, noncall.

BofA Securities priced for the Virginia Housing Development Authority (Aaa/AAA//) $150 million of taxable commonwealth mortgage bonds, 2023 Series B, with all bonds pricing at par: 5.456s of 11/2024, 5.728s of 5/2028, 5.778s of 11/2028, 6.141s of 5/2033, 6.171s of 11/2033, 6.241s of 11/2038, 6.404s of 11/2043, 6.514s of 11/2048 and 6.534s of 11/2053, callable 5/1/2032.

BofA Securities also priced for the authority $100 million of non-AMT commonwealth mortgage bonds, 2023 Series A, with all bonds pricing at par: 3.8s of 11/2024, 4s of 5/2028, 4.05s of 11/2028, 4.55s of 5/2033, 4.55s of 11/2033, 5s of 11/2038, 5.125s of 11/2043, 5.25s of 11/2048 and 5.3s of 11/2053, callable 5/1/2032.

September redux

In September, tax-exempts “posted negative returns and underperformed Treasuries across the curve … on weak technical factors,” said Peter Block, managing director of credit strategy at Ramirez & Co.

These factors include muni mutual fund outflows, expectations of higher-for-longer rates from the Fed, negative returns year-to-date, low absolute and relative value and curve inversion through 13 years, he said.

The Refinitiv MMD curve was cut by an average of more than 50 basis points in September. This bear flattened 2s30s by -7 basis points to +68 basis points, he said

The Refinitiv MMD 2s10s remains inverted at -21 basis points, Block noted.

SIFMA was lower by -8 basis points in September to 3.98%, or 100% of 16-year MMD, exacerbating weak demand, he said.

Despite underperformance year-to-date, he said muni-USTs ratios “remain fair-to-rich heading into October with only small pockets of value by name and structure.”

For the fourth quarter, Block estimates $83 billion of gross supply, meaning 2023 will see $350 billion of issuance, which down 8.9% year-over-year. The $83 billion figure includes $38 billion of issuance in October.

For this month, net supply will be positive at $11 billion, which is around 71% of gross supply. This will turn negative in November and December at negative $15 billion, or 135% of gross supply.

Demand for tax-exempts remained weak last month as investors pulled $2.18 billion from muni mutual funds in September, with the first three quarters seeing outflows total $9.8 billion, according to Refinitiv Lipper.

Block expects “continued weak demand in October, exacerbated by positive net supply.”

In October, munis should continue to underperform USTs on “weak” technical factors, he said. There is the potential for recovery in November and December “to the extent rate fears subside and given expected negative net supply,” he said.

Secondary trading

California 5s of 2024 at 3.74%-3.60% versus 3.28%-3.29% on 9/22. Washington 5s of 2025 at 3.83%-3.80%. Maryland 5s of 2025 at 3.75%.

Maryland 5s of 2028 at 3.52%-3.51%. Georgia 5s of 2028 at 3.44%-3.42%. NYC 5s of 2029 at 3.66% versus 3.76% Tuesday.

Illinois Finance Authority 5s of 2032 at 3.74%-3.70%. Minnesota 5s of 2033 at 3.60% versus 3.57% Tuesday. NYC 5s of 2034 at 3.86%-3.81%.

Washington 5s of 2045 at 4.52% versus 4.46%-4.44% on 9/26. NYC TFA 5s of 2048 at 4.80% versus 4.36%-4.37% on 9/19.

AAA scales

Refinitiv MMD’s scale was bumped up to three basis points: The one-year was at 3.74% (unch) and 3.66% (-3) in two years. The five-year was at 3.43% (-2), the 10-year at 3.50% (unch) and the 30-year at 4.39% (unch) at 3 p.m.

The ICE AAA yield curve was slightly firmer outside of three years: 3.75% (+1) in 2024 and 3.70% (+1) in 2025. The five-year was at 3.46% (-2), the 10-year was at 3.49% (-1) and the 30-year was at 4.39% (-1) at 4 p.m.

The S&P Global Market Intelligence municipal curve was bumped up to three basis points: The one-year was at 3.77% (unch) in 2024 and 3.69% (-3) in 2025. The five-year was at 3.47% (-2), the 10-year was at 3.51% (unch) and the 30-year yield was at 4.40% (unch), according to a 3 p.m. read.

Bloomberg BVAL was cut bumped up to one basis point: 3.78% (unch) in 2024 and 3.70% (-1) in 2025. The five-year at 3.43% (-1), the 10-year at 3.50% (-1) and the 30-year at 4.43% (-1) at 4 p.m.

Treasuries were firmer.

The two-year UST was yielding 5.045% (-11), the three-year was at 4.850% (-10), the five-year at 4.713% (-9), the 10-year at 4.724% (-8), the 20-year at 5.054% (-8) and the 30-year Treasury was yielding 4.857% (-8) near the close.

NYS plans $9B of bond sales in Q4

New York State, New York City and their governmental authorities plan to sell $9.11 billion of bonds in the fourth quarter, state comptroller Thomas DiNapoli announced Wednesday.

The sales include $6.43 billion of new-money bonds and $2.68 billion of refunding bonds.

About $7.6 billion is scheduled for issuance this month, consisting of $5.74 billion of new-money and $1.86 billion of refunding bonds.

Roughly $125 million is scheduled for November, all of which is for new-money purposes.

In December, $1.38 billion is expected to be issued, $560 million of which will be new money and $820 million of refundings.

The anticipated sales compare to past planned sales of $3.38 billion in the third quarter and $5.65 billion in the fourth quarter of 2022.

The upcoming calendar includes anticipated bond sales by NYC, the Empire State Development Corp., the Environmental Facilities Corp., the NYC Housing Development Corp., the NYC Transitional Finance Authority, the New York Power Authority, the NYS Housing Finance Agency, the NYS Thruway Authority, the New York Transportation Development Corp., the State of New York Mortgage Agency, the Triborough Bridge and Tunnel Authority and the Utility Debt Securitization Authority.

Primary to come

Fort Lauderdale, Fla. (Aa1/AA+//) is on tap to price $504.9 million of water and sewer revenue bonds for the Prospect Lake Water Treatment Plant Project Thursday. Morgan Stanley & Co. LLC.

The Alameda County, Calif., (Aa1/AA+/AA+/) is set to price $197.3 million of lease revenue refunding bonds for the Highland Hospital Project Thursday. Serials 2024-2034. Citigroup Global Markets Inc.

The Illinois Housing Development Authority (Aaa///) is set to price $178.7 million of revenue bonds Thursday. Serials 2025-2035, terms 2038, 2043, 2047 2053. Wells Fargo Bank.

The Florida Housing Finance Corp. (Aaa///) is set to price $100 million of Series 6 taxable homeowner mortgage revenue bonds Thursday. Serials 2025-2033, terms 2038, 2043, 2048, 2054, 2055. Citigroup Global Markets Inc.

Chip Barnett contributed to this story.