Munis were weaker Tuesday, but outperformed a U.S. Treasury selloff. Equities sold off as well.

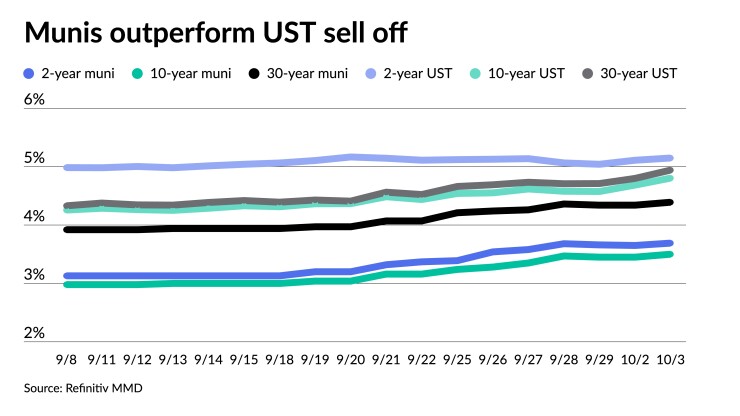

Triple-A yields rose anywhere from two to eight basis points while UST saw yields rise by as much as 13 basis points out long.

The two-year muni-to-Treasury ratio Tuesday was at 72%, the three-year was at 72%, the five-year at 72%, the 10-year at 73% and the 30-year at 89%, according to Refinitiv Municipal Market Data’s 3 p.m., ET, read. ICE Data Services had the two-year at 72%, the three-year at 73%, the five-year at 73%, the 10-year at 75% and the 30-year at 91% at 4 p.m.

UST rates are driving all things in the muni market, said Jon Mondillo, head of North American Fixed Income at abrdn.

Over the last two weeks, he said USTs have risen 88 basis points at two years, 35 basis points at five years, 49 basis points at 10 years and 55 basis points at 30 years.

The rise in UST yields has “contributed to the pain that’s been felt in this market,” he said.

Triple-A yield curves in September rose 45 to 53 basis points, according to Refinitiv MMD.

“That’s contributed to a really a huge give up in our total return on a year-to-date basis,” he said.

Due to September’s losses, the Bloomberg Municipal Index is now returning -1.50% year-to-date.

Despite all of the negatives, Mondillo believes the worst is behind us. While munis sold off last week, there have been smaller cuts to AAA curves Monday and Tuesday.

He said the expected issuance for October will be met with more than enough demand from maturing securities as well as coupon payments.

Rising yields present an opportunity, said Cooper Howard, a fixed-income strategist at Charles Schwab.

He believes “munis are attractive given the recent move up in yields and seasonal factors that should be supportive of total returns going forward.”

For an investor in the top tax bracket, Howard said the taxable-equivalent yield for the broad index is around 7.4%.

Fund flows, though, are more of “an unknown or question mark … which has been an impediment to overall total return thus far,” Mondillo said.

He expects fund flows to continue to be “a bit negative” in the fourth quarter, particularly October, but that “overall performance in the municipal bond market should be a bit better in October than it was in September.”

This month, he said issuance will be a little bit lighter than market expectations given “the sticker shock and the rate moves that we’ve gone through over the last 30 days.”

Therefore, he said it’s likely some of that issuance sitting on the sidelines.

But the “healthy amount of bonds coming due with coupon payments should help performance,” he noted.

In November and December, he said it’s unclear where supply will fall.

“There’s only so long municipalities can wait to issue debt,” he said. “While some of the municipalities that we’ve seen have gone to the sidelines and taking a weekly approach, which has suppressed supply thus far this year.”

However, he noted there’s the possibility that supply will tick up in December, at least during the first two weeks of the month relative to previous years as “municipalities are really forced to come to market at these elevated levels.

Jefferies preliminarily priced for the San Diego County Regional Airport Authority (A1//AA-/) $1.063 billion of senior airport revenue bonds on behalf of the San Diego International Airport. The first tranche, $75.190 million of governmental/non-AMT bonds, Series 2023A, with 5s of 7/2024 at 3.80%, 5s of 2028 at 3.53%, 5s of 2033 at 3.64%, 5s of 2038 at 4.24%, 5s of 2043 at 4.55%, 5s of 2048 at 4.73%, 5s of 2053 at 4.79% and 5s of 2058 at 4.89%, callable 7/1/2033.

The second tranche, $987.680 million of private activity/AMT bonds, Series 2023B, saw 5s of 7/2028 at 4.41%, 5s of 2033 at 4.50%, 5.25s of2038 at 4.94%, 5s of 2043 at 5.10%, 5s of 2053 at 5.24%, 5.25s of 2058 at 5.34%, callable 7/1/2033.

Goldman Sachs priced and repriced for the Omaha Public Power District (Aa2/AA//) $548.650 million of electric system revenue bonds, with yields bumped up to five basis points upon repricing. The first tranche, $359.940 million of 2023 Series A, saw 5s of 2/2025 at 3.85% (-3), 5s of 2028 at 3.61% (-5), 5s of 2033 at 3.76% (unch), 5s of 2038 at 4.24% (-5), 5s of 2043 at 4.57% (unch), 5.25s of 2048 at 4.69% (unch) and 5.25s of 2053 at 4.75% (unch), callable 2/1/2033.

The second tranche, $188.710 million of 2023 Series B, 5s of 2/2025 at 3.88%, 5s of 2028 at 3.66%, 5s of 2033 at 3.76%, 5s of 2038 at 4.29%, 5s of 2043 at 4.57%, 5.25s of 2048 at 4.69% and 5.25s of 2053 at 4.75%, callable 2/1/2033.

Wells Fargo Bank priced for the Illinois Housing Development Authority (Aaa///) $178.750 million of non-AMT social revenue bonds, 2023 Series K, with all bonds pricing at par – 3.95s of 4/2025, 4.25s of 4/2028, 4.3s of 10/2028, 4.8s of 4/2033, 4/8s of 10/2033, 4.95s of 10/2038, 5.25s of 10/2043 and 5.35s of 4/2047 – except 6.25s of 10/2053 at 5.01%, callable 10/1/2032.

In the competitive market, Montgomery County, Pennsylvania (Aaa///), $141.395 million of GOs, Series 2023A, saw 5s of 10/2024 at 3.76%, 5s of 2028 at 3.46%, 5s of 2033 at 3.55%, 5s of 2038 at 4.18% and 5s of 2043 at 4.43%, callable 10/1/2031.

The county also $14.210 million of GOs, Series 2023B, saw 5s of 10/2024 at 3.76%, 5s of 2028 at 3.46%, 5s of 2033 at 3.55%, 5s of 2038 at 4.20% and 5s of 2043 at 4.40%, callable 10/1/2031.

Secondary trading

Oregon 5s of 2024 at 3.74%. Washington 5s of 2024 at 3.79%. Maryland 5s of 2024 at 3.76%-3.74%.

Maryland 5s of 2028 at 3.50%. NYC 5s of 2028 at 3.74%-3.72%. Board of Regents of the University of Texas System 5s of 2029 at 3.62%-3.61% versus 3.60% Friday and 3.16% on 9/18.

Minnesota 5s of 2033 at 3.57%. Texas Water Development Board 5s of 2034 at 3.69%-3.64% versus 3.67% original on Thursday. California 5s of 2035 at 3.77% versus 3.74% Friday and 3.66% on 9/27.

Massachusetts Transportation Fund 5s of 2051 at 4.65% versus 4.63%-4.61% Monday and 4.53% Friday. San Jose Financing Authority 5s of 2053 at 4.47%-4.46% versus 4.35% Friday and 4.21%-4.08% on 9/27. NYC Municipal Water Finance Authority 5s of 2053 at 4.76%-4.77% versus 4.82%-4.79% original on Friday.

AAA scales

Refinitiv MMD’s scale was cut four to five basis points: The one-year was at 3.74% (+4) and 3.69% (+4) in two years. The five-year was at 3.45% (+4), the 10-year at 3.50% (+5) and the 30-year at 4.39% (+5) at 3 p.m.

The ICE AAA yield curve was cut one to eight basis points: 3.74% (+1) in 2024 and 3.69% (+2) in 2025. The five-year was at 3.48% (+8), the 10-year was at 3.50% (+8) and the 30-year was at 4.40% (+5) at 4 p.m.

The S&P Global Market Intelligence municipal curve was cut six basis points: The one-year was at 3.77% (+6) in 2024 and 3.72% (+6) in 2025. The five-year was at 3.49% (+6), the 10-year was at 3.51% (+6) and the 30-year yield was at 4.40% (+6), according to a 3 p.m. read.

Bloomberg BVAL was cut five to six basis points: 3.78% (+5) in 2024 and 3.71% (+5) in 2025. The five-year at 3.43% (+5), the 10-year at 3.50% (+5) and the 30-year at 4.44% (+6) at 4 p.m.

Treasuries sold off.

The two-year UST was yielding 5.150% (+4), the three-year was at 4.954% (+7), the five-year at 4.804% (+9), the 10-year at 4.805% (+12), the 20-year at 5.132% (+13) and the 30-year Treasury was yielding 4.937% (+14) near the close.

Primary to come

New York City (Aa2/AA/AA/AA+/) is set to price $965 million of taxable general obligation bonds Wednesday. Serials, 2025-2038, terms 2046, 2053. Barclays Capital.

Fort Lauderdale, Fla. (Aa1/AA+//) is on tap to price $504.9 million of water and sewer revenue bonds for the Prospect Lake Water Treatment Plant Project Thursday. Morgan Stanley & Co. LLC.

South Carolina’s Building Equity Sooner for Tomorrow (Aa2///) is set to price $275.8 million of installment purchase revenue refunding bonds on behalf of the School District of Greenville County, S.C., Wednesday. J.P. Morgan Securities LLC.

The Alameda County, Calif., (Aa1/AA+/AA+/) is set to price $197.3 million of lease revenue refunding bonds for the Highland Hospital Project Thursday. Serials 2024-2034. Citigroup Global Markets Inc.

The Illinois Housing Development Authority (Aaa///) is set to price $178.7 million of revenue bonds Thursday. Serials 2025-2035, terms 2038, 2043, 2047 2053. Wells Fargo Bank.

The Virginia Housing Development Authority (Aaa/AAA//) is set to issue $150 million of taxable commonwealth mortgage bonds Wednesday. Serials 2024-2033, terms 2038, 2043, 2048, 2053. BofA Securities. It will also issue $100 million of non-AMT commonwealth mortgage bonds Wednesday. Serials 2024-2035, terms in 2038, 2043, 2048, 2053.

The New York State Housing Finance Agency (Aa2///) is set to price $149.5 million of affordable housing sustainability revenue bonds Wednesday. Serials 2024-2035, terms 2038, 2043, 2048, 2053, 2058, 2062 2063. Ramirez & Co., Inc.

The Florida Housing Finance Corp. (Aaa///) is set to price $100 million of Series 6 taxable homeowner mortgage revenue bonds Thursday. Serials 2025-2033, terms 2038, 2043, 2048, 2054, 2055. Citigroup Global Markets Inc.

Competitive

California (Aa2/AA-/AA/) is set to sell a total of $943 million of taxable GOs Wednesday — $440 million maturing serially in 2031 and 2041 and $502 million maturing serially in 2028 and 2031.