Municipals were steady Wednesday as U.S. Treasuries were mixed fiollowing the Fed’s decision to hold interest rates. Equities ended the trading session down.

As was expected, the FOMC held rates in a range between 5.25% and 5.50%, but the dot plot in the Summary of Economic Projections showed 12 of 19 members expect another 25-basis-point rate hike this year.

In his press conference, Fed Chair Jerome Powell, said the panel will be data dependent and “doesn’t want to jump to conclusions” and needs to be confident it is “at a stance that will bring inflation down to 2%.” The additional rate hike possibility is the result of stronger economic activity, he said.

A soft landing is not his base case, Powell said, but it is a “plausible outcome.”

For municipals, the reaction was muted with triple-A yields weaker on the short end to mostly little changed, depending on the scale, leading muni-UST ratios to hold steady.

The two-year muni-to-Treasury ratio Wednesday was at 62%, the three-year was at 64%, the five-year at 66%, the 10-year at 70% and the 30-year at 90%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 64%, the three-year at 65%, the five-year at 65%, the 10-year at 69% and the 30-year at 90% at 4 p.m.

Heading into September, it has been quieter and slower for the muni market, “but for all intents and purposes, munis are running on all cylinders,” said Jeff Timlin, a managing partner at Sage Advisory.

“They’re in a really good place,” he said. “Obviously, we had this big reset … but since then, spreads have compressed back down to fair value if maybe not richer territory.”

Fundamentals also look as good “at least in terms of liquidity ratios and things of that nature, and even on the pension front, although it’s far from being fixed,” he noted.

But for all the positives, issuance remains down year-over-year and one of the main drivers of new issuance is absolute rates, he said.

When rates were as low as 1% and in some places on the curve, near zero, “we had record issuance.”

This rise in rates that began in early 2022 removed a significant amount of refunding deals and there is hesitancy from issuers “to take on that interest cost.”

Furthermore, the economy has been strong over the past decade, where municipalities “have gotten then into a good fiscal situation so they haven’t had to issue as much debt and can fund projects through current fundings in the excess budget reserves,” he said.

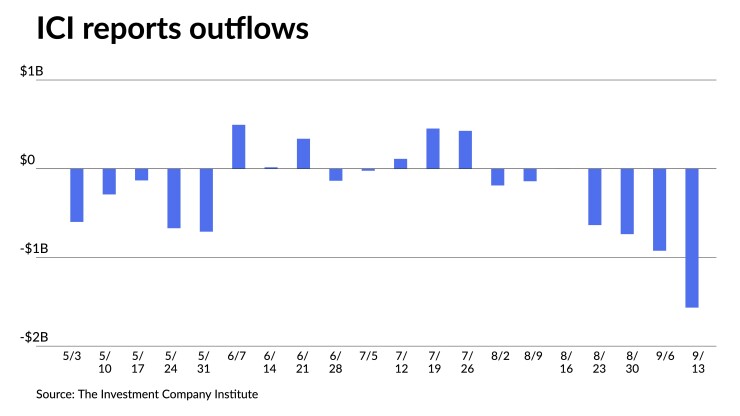

Additionally, there are still net negative outflows from muni mutual funds.

The Investment Company Institute Wednesday reported investors pulled $1.566 billion from municipal bond mutual funds in the week ending Sept. 13 after $925 million of outflows the previous week.

However, Timlin noted that is being offset in less publicized numbers for separately managed accounts and exchange-traded funds.

For the most recent reporting week, ETFs saw inflows of $852 million after $222 million of outflows the week prior, according to ICI.

“So money’s flowing out of the mutual fund complex into the ETF complex as well as the SMAs,” he said.

However, there is still strong demand there across the board.

“There’s ebbs and flows of less liquidity, but it seems generally speaking new-issue market is extremely well bid across the board, particularly if it’s priced correctly,” he said. As dealer inventory has been slowly creeping down, “that’s an indicator of people just kind of having to put money to work.”

Technical factors will be a big help with the buyers’ market in Q3, he said. Going into the second half of Q4, there will be a more stable market with rates a little bit lower as participants reposition.

For the remainder of the year, he said munis may “initially be heading a little bit higher in rates, following Treasuries with the uncertainty there.”

The market still has this relatively strong economic backdrop.

There are some challenges here and there, but “holistically it seems to be the factors that influence rates are still prevalent in the market,” he said.

There will be a short period of time where rates head higher but toward the end of the year, he said the markets will settle down during the holiday season.

During that period, there “are less market makers and things get pushed off to 2024, including issuance,” he said.

In the primary market Wednesday, Citigroup Global Markets priced for the San Diego Unified School District (Aa2//AAA/AAA/) $670 million of 2023 GO dedicated unlimited ad valorem property tax bonds. The first tranche, $161 million of green Election of 2018 bonds, Series G-2, saw 5s of 7/2025 at 3.08% and 5s of 2028 at 2.88%, noncall.

The second tranche, $189 million of green Election of 2018 bonds, Series G-3, saw 5s of 7/2041 at 3.78%, 5s of 2043 at 3.90% and 4s of 2053 at 4.42%, callable 7/1/2033.

The third tranche, $25 million of sustainability Election of 2022 bonds, Series A-2, saw 5s of 7/2024 at 3.18% and 5s of 2028 at 2.88%, noncall.

The fourth tranche, $295 million of sustainability Election of 2022 bonds, Series A-3, saw 5s of 7/2048 at 4.18% and 4s of 2053 at 4.42%, callable 7/1/2033.

In the competitive market, Cape May County, New Jersey (Aa1///), sold $96 million of GOs, to Citigroup Global Markets, with 4s of 9/2024 at 3.20%, 4s of 2028 at 2.90%, 4s of 2033 at 3.00% and 4s of 2038 at 3.90%, callable 9/15/2030.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.30% and 3.20% in two years. The five-year was at 2.98%, the 10-year at 3.04% and the 30-year at 3.97% at 3 p.m.

The ICE AAA yield curve was cut up three basis points: 3.35% (+3) in 2024 and 3.26% (+3) in 2025. The five-year was at 2.98% (unch), the 10-year was at 3.00% (-1) and the 30-year was at 3.99% (unch) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was unchanged: 3.31% in 2024 and 3.20% in 2025. The five-year was at 2.99%, the 10-year was at 3.04% and the 30-year yield was at 3.97%, according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 3.29% in 2024 and 3.20% in 2025. The five-year at 2.94%, the 10-year at 2.98% and the 30-year at 3.95% at 4 p.m.

Treasuries were mixed.

The two-year UST was yielding 5.165% (+6), the three-year was at 4.839% (+5), the five-year at 4.550% (+3), the 10-year at 4.366% (flat), the 20-year at 4.600% (-1) and the 30-year Treasury was yielding 4.409% (-2) near the close.

No surprises from FOMC

The panel, in keeping with the higher-for-longer narrative the Fed has been promoting, raised its median projection for next year to 5.1%, a half-point higher than the previous estimate. The dot plot suggests a 3.9% rate at the end of 2025 and a 2.9% target at the end of 2026.

The projections show growth, as measured by GDP, at 2.1% this year, 1.5% next year and 1.8% in subsequent years. The previous SEP had growth at 1.0% this year, 1.1% next year and 1.8% in 2025.

Inflation expectations were lifted a tick to 3.3% for this year, held steady at 2.5% next year, and raised to 2.2% from 2.1% in 2025. The new projections, which cover 2026 for the first time, project 2.0% inflation in 2026.

Unemployment projections were cut to 3.8% for this year, 4.1% the following two years and 4.0% in 2026.

Olu Sonola, Fitch head of U.S. economics, called “consequential” the panel’s dot plot suggesting another hike this year.

“The message conveyed in their upward revision to growth and their downward revision to the unemployment rate in 2024 clearly indicate a Fed that has dialed up their expectation for a soft landing, despite higher for longer rates,” Sonola said. “We think 2024 may present a different set of realities that contradict the Fed’s expectation.”

Despite the projection, Thomas Holzheu, Swiss Re’s chief economist for the Americas, said, “We believe the Fed has reached its terminal policy rate of this cycle, but the risk of further inflation surprises and ongoing strength in economic activity suggests policymakers will remain hawkish in their communications and tighten further if appropriate.”

“We believe the Fed would prefer to have an additional hike in the dots and not need to execute one, rather than need to execute an additional hike and not have one in the dots,” said Josh Jamner, investment strategy analyst at ClearBridge Investments.

The dot plot showing fewer cuts next year could be the Fed “erring on the side of caution and not wanting to overpromise and then under-deliver.”

The post-meeting statement “was more hawkish than expected,” according to Alexandra Wilson-Elizondo, deputy CIO, multi-asset strategies at Goldman Sachs Asset Management. ”The main risk remains tarnishing their largest asset, anti-inflation credibility, which warrants favoring a hawkishness reaction function.”

“It’s noteworthy that the policy rate is projected to remain above its longer-run level through the end of 2026,” said Michael Gregory, deputy chief economist at BMO Capital Markets. “Powell said the current neutral rate could be higher than its longer-run mark, which it would be if inflation is proving to be more stubborn than expected. Meanwhile, five participants now project that the longer-run level rests above 2.75%, compared to three before. We have an inkling that this will be a theme in upcoming SEPs.”

Primary on Tuesday

Goldman Sachs priced for the Patriots Energy Group Financing Agency (A1///) $611.420 million of gas supply revenue bonds. The first tranche, $599.155 million of Series 2023A-1 bonds, saw 5.25s of 10/2054 with a mandatory tender date of 8/1/2031 at 4.98%, callable 5/1/2031.

The second tranche, $12.265 million of Series 2023A-2 bonds, saw 6.5s of 8/2031 price at par.